Introduction: This Is Not an Ethics Story — It’s a Systems Story

Most trust accounting failures are not sudden.

They don’t start with fraud.

They start with:

- loose processes

- informal habits

- small shortcuts

And then, over time:

👉 those gaps compound into exposure.

A recent West Virginia case involving allegations of mishandling client funds offers a clear example of how operational weaknesses can escalate into serious consequences.

For context, you can review the original reporting here:

👉 https://www.legalnewsline.com/west-virginia-record/harris-indicted-on-42-counts-of-mishandling-client-funds/article_0e6f6af2-aab1-42ce-8679-4adaf39ac152.html

This article is not about the allegations themselves.

It’s about what lawyers should take away from them.

The Core Reality: Trust Accounting Is an Operational Discipline

Every lawyer knows Rule 1.15.

But knowing the rule is not the same as implementing it.

Trust accounting requires:

- structured workflows

- documented controls

- consistent reconciliation

- clear separation of funds

Without those, compliance becomes dependent on:

- memory

- intention

- “what usually works”

That’s where risk begins.

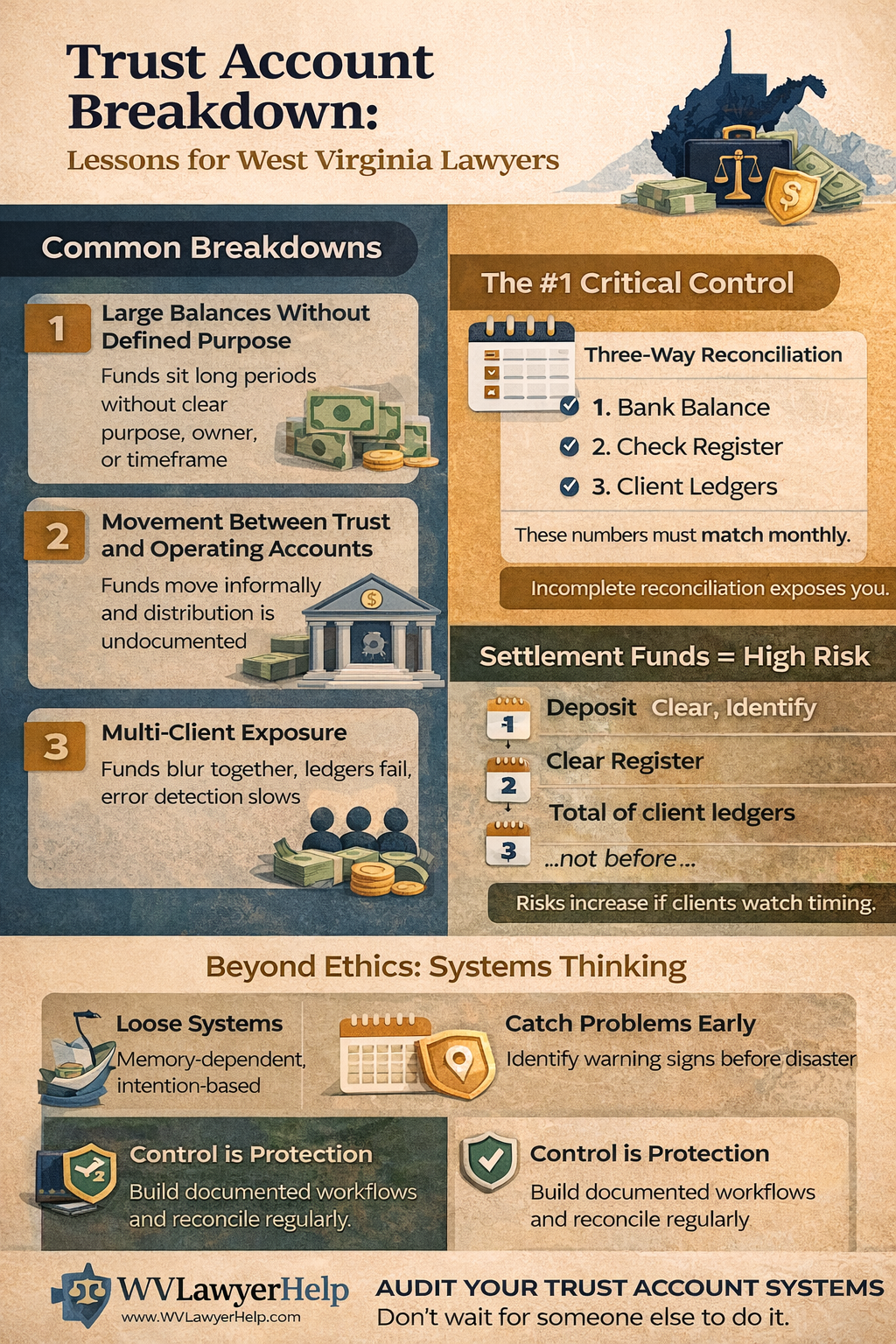

Pattern #1: Large Balances Without Defined Purpose

In many trust accounting failures, funds remain in trust for extended periods.

This creates ambiguity:

- What is this money for?

- Who does it belong to?

- Why hasn’t it moved?

Best practice:

👉 Every dollar in trust should have:

- a defined owner

- a defined purpose

- a defined timeline

Anything else is exposure.

Pattern #2: Movement Between Trust and Operating Accounts

This is where systems either hold — or fail.

Funds should only move:

- when fees are earned

- when expenses are incurred

- when distribution is documented

Breakdowns occur when:

- transfers happen informally

- documentation lags behind

- timing is inconsistent

👉 This is how small issues become large ones.

Pattern #3: Multi-Client Exposure

One of the most dangerous breakdowns occurs when:

👉 The system stops treating each client separately

Instead:

- funds blur together

- ledgers become unreliable

- reconciliation becomes difficult

At that point:

- errors multiply

- detection slows

- risk accelerates

The Most Important Control: Three-Way Reconciliation

If there is one habit that prevents disaster, it is this:

Monthly Three-Way Reconciliation

You must reconcile:

- Bank balance

- Check register

- Total of client ledgers

If these do not match:

👉 You have a problem.

And the longer it goes unresolved, the harder it becomes to fix.

Settlement Funds: The Highest-Risk Event in a Law Firm

Settlement disbursement is where trust accounting is most visible.

It is also where failures are most likely to be discovered.

Why?

Because:

- clients are watching

- amounts are large

- expectations are high

Proper Workflow

- Deposit funds

- Confirm clearance

- Identify all obligations

- Prepare written settlement statement

- Disburse

No shortcuts.

Common Failure Points

- disbursing before funds clear

- incomplete accounting

- verbal explanations instead of documentation

👉 These are operational failures, not ethical gray areas.

The Solo & Small Firm Reality

In smaller firms, risk is amplified.

Why?

Because:

- fewer controls

- limited separation of duties

- heavier reliance on the attorney

What You Need Instead

A system:

- documented workflows

- monthly reconciliation schedule

- clear deposit/disbursement rules

- review checkpoints

Because without structure:

👉 trust accounting becomes personality-driven

The Misconception: “Good Intentions Are Enough”

They’re not.

Trust accounting is not about:

- honesty

- effort

- experience

It is about:

👉 repeatability and documentation

Every dollar should be:

- traceable

- explainable

- supported

Early Warning Signs Inside a Firm

Before a major issue appears, there are signals:

- reconciliation is skipped or delayed

- ledgers don’t match balances

- funds sit without clear purpose

- documentation is incomplete

These are not minor issues.

They are early-stage failures.

Final Insight: Audit Yourself Before Someone Else Does

Most trust accounting disasters:

- build slowly

- remain hidden

- become visible too late

The solution is simple — but not easy:

👉 build systems that catch problems early

Because once trust accounting breaks:

👉 it is rarely just an accounting problem

Closing Thought

If your firm’s trust accounting depends on:

- memory

- trust

- informal processes

It is already at risk.

Because in trust accounting:

👉 control is protection